Renewable energy has shown that concern for the environment per se does not count for much unless there is a business to be built. Carbon capture (which includes transportation and storage) may well traverse the path already drawn by renewable energy, but hopefully it will be faster and shorter. A Mumbai-based startup’s innovation shows promise

There is a tacit assumption that the goal of net zero, once reached, will stay and reproduce itself continuously. In conferences after conferences, you hear world leaders talking about reaching the goal of net zero without also mentioning that it needs to be maintained. It is another matter that the goal itself has been pushed further in time.

Net zero refers to emissions cancelling out each other – those which are ‘put out there’ in the atmosphere and those which are removed. As we can see, it is a game of numbers. If the emissions emanating through economic activities decline slowly, the efficiency in removal will have to compensate, which calls for technological improvements and investments.

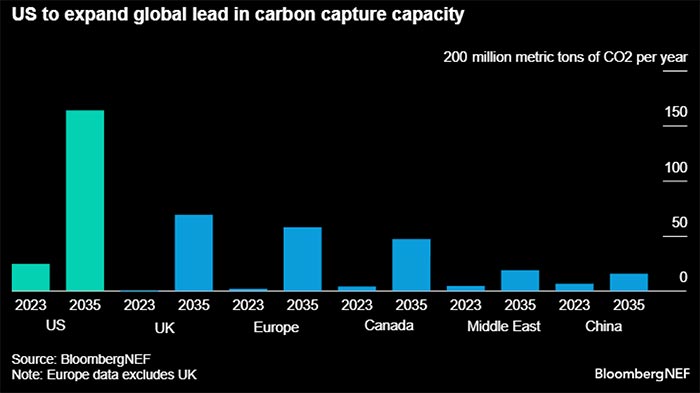

Net zero, even assuming that countries are serious about the goal, is the result of the combined effect of both. If the negative is strong, so has to be the positive. This is what makes carbon capture so important. As BloombergNEF notes, “Carbon is captured mainly from natural gas processing and utilized for enhanced oil recovery currently”, https://about.bnef.com/blog/us-is-set-to-expand-global-lead-in-capturing-carbon/. As capacity expands, carbon will mostly be captured from the hydrogen industry, with the power sector being the second largest segment.

If we suspend thinking on emissions emanating and focus on their removal, we see a stark truth: just as it happened in the case of renewable energy, emissions will not gather momentum unless people see a business potential in it. Renewable energy is a big business today and both old and new companies are investing substantial sums of money in producing renewable energy and in building the corollary facilities in grid infrastructure (because sources of renewable energy have to be connected to the power grids).

Renewable Energy investments

The International Energy Agency, in its lates report, observes that “Global energy investment is set to exceed USD 3 trillion for the first time in 2024, with USD 2 trillion going to clean energy technologies and infrastructure. Investment in clean energy has accelerated since 2020, and spending on renewable power, grids and storage is now higher than total spending on oil, gas, and coal” (https://www.iea.org/reports/world-energy-investment-2024/overview-and-key-findings).

Let me quote in full the next paragraph to portray the current and developing scenario: “The annual World Energy Investment report has consistently warned of energy investment flow imbalances, particularly insufficient clean energy investments in EMDE outside China. There are tentative signs of a pick-up in these investments: in our assessment, clean energy investments are set to approach USD 320 billion in 2024, up by more 50% since 2020. This is similar to the growth seen in advanced economies (+50%), although trailing China (+75%). The gains primarily come from higher investments in renewable power, now representing half of all power sector investments in these economies. Progress in India, Brazil, parts of Southeast Asia and Africa reflects new policy initiatives, well-managed public tenders, and improved grid infrastructure. Africa’s clean energy investments in 2024, at over USD 40 billion, are nearly double those in 2020”.

Investment in carbon capture

TT Consulting, active in the area of carbon capture, says that “Carbon dioxide capture and storage (CCS) technology has emerged as a critical component in the global strategy to mitigate climate change. CCS involves capturing CO2 emissions from industrial sources, transporting the captured CO2, and securely storing it underground to prevent it from entering the atmosphere” – (https://ttconsultants.com/the-future-of-co2-capture-patent-landscape-market-dynamics-and-technological-innovations/).

While this is certainly true, the investments into all three aspects of carbon capture – capture, transportation, storage – is yet to reach the levels that RE can boast of. According to Statista, investment in carbon capture was $11.3 billion in 2023 from $0.8 billion in 2018 – https://www.statista.com/statistics/1489995/carbon-capture-and-storage-global-investments-per-year/.

According to BloombergNEF, the US, which leads the carbon capture industry, aims to increase its capacity sevenfold by 2035, when it will “have the capacity to capture as much as 164 million tons of carbon by 2035 — almost equivalent to the next three markets combined” (https://about.bnef.com/blog/us-is-set-to-expand-global-lead-in-capturing-carbon/). According to Wood Mackenzie’s report CCUS: 10-year market forecast , “By 2034, global carbon capture capacity will reach 440 Mtpa and storage capacity will reach 664 Mtpa, requiring US$ 196 billion in total investment”. Nearly half of the investment goes into CO2 capture, with US$53 billion going into transport and US$43 billion into storage. Geographically, there is a substantial imbalance as about 70% of the investment is expected to be in North America and Europe – https://www.woodmac.com/press-releases/2024-press-releases/global-ccus-investment-requires-us$-196b-through-2034-according-to-wood-mackenzie/.

Miles to go

Of course, this is encouraging if you looked at the 2018 figures, but we have a long way to go. As one article observes, “The number of projects in advanced development stages saw a 55% increase from 2022 to 2024, and early-stage projects jumped by 64%. However, achieving climate goals requires a monumental increase in storage capacity. Estimates from the IEA and IPCC suggest that global CO2 storage must reach 1 Gtpa (gigatonne per annum) by 2030, and 6 Gtpa by 2050. The current pace of growth, while promising, may not be sufficient to meet these targets, especially given the long lead time for CCUS (carbon capture utilisation and storage) projects—typically 6 to 10 years from inception to operation.

One of the deterrents is the high cost of investment, which is also an entry barrier. There may be a ray of hope, though. A Mumbai-based startup, UrjanovaC, “has developed an aqueous-based CO2 capture technology comprising a new catalyst that is robust, cost-effective, and scalable. This technology has the capability to capture CO2 in industrial wastewater”. This innovation is the result of cooperation among a government department, an academic institution and a startup – research work at the Department of Science and Technology supported National Centre of Excellence in Carbon Capture and Utilization at IIT Bombay. Moreover, IIT Bombay’s Society For Innovation & Entrepreneurship’s The Technology Business Incubator nurtured UrjanovaC, whose founders, Prof. Vikram Vishal and Prof. Arnab Dutta, are faculty members at IIT Bombay.

Useful resources

https://www.iea.org/energy-system/carbon-capture-utilisation-and-storage